Audit Procedures for Cash and Cash Equivalents

5 The high value and liquid nature of many financial. AUDIT RISKS AND AUDIT PROCEDURES FOR CASH AND BANK ACCOUNTS.

Audit Cash Cash Equivalents Youtube

It is considered high risk for both company and auditors.

. Cash and Cash Equivalent is scoped under IAS 7 Statements of Cash Flows. Retain documentation for all items of expenditure. Auditor has to check if the cash on hand.

This CPE course can be purchased individually or as part of the Audit Staff Essentials - New Staff. Audit Procedures for Cash and Cash Equivalents Audit. View Audit Procedures for Cash and Cash Equivalentsdocx from ACCOUNTANC ACCOUNTANC at University of Santo Tomas.

A short summary of this paper. Practical Application staff training bundle. The first is cash which comprises.

2 Full PDFs related to. Gain an understanding of the. 2 Summarized Business Cycle Cash and Cash equivalent.

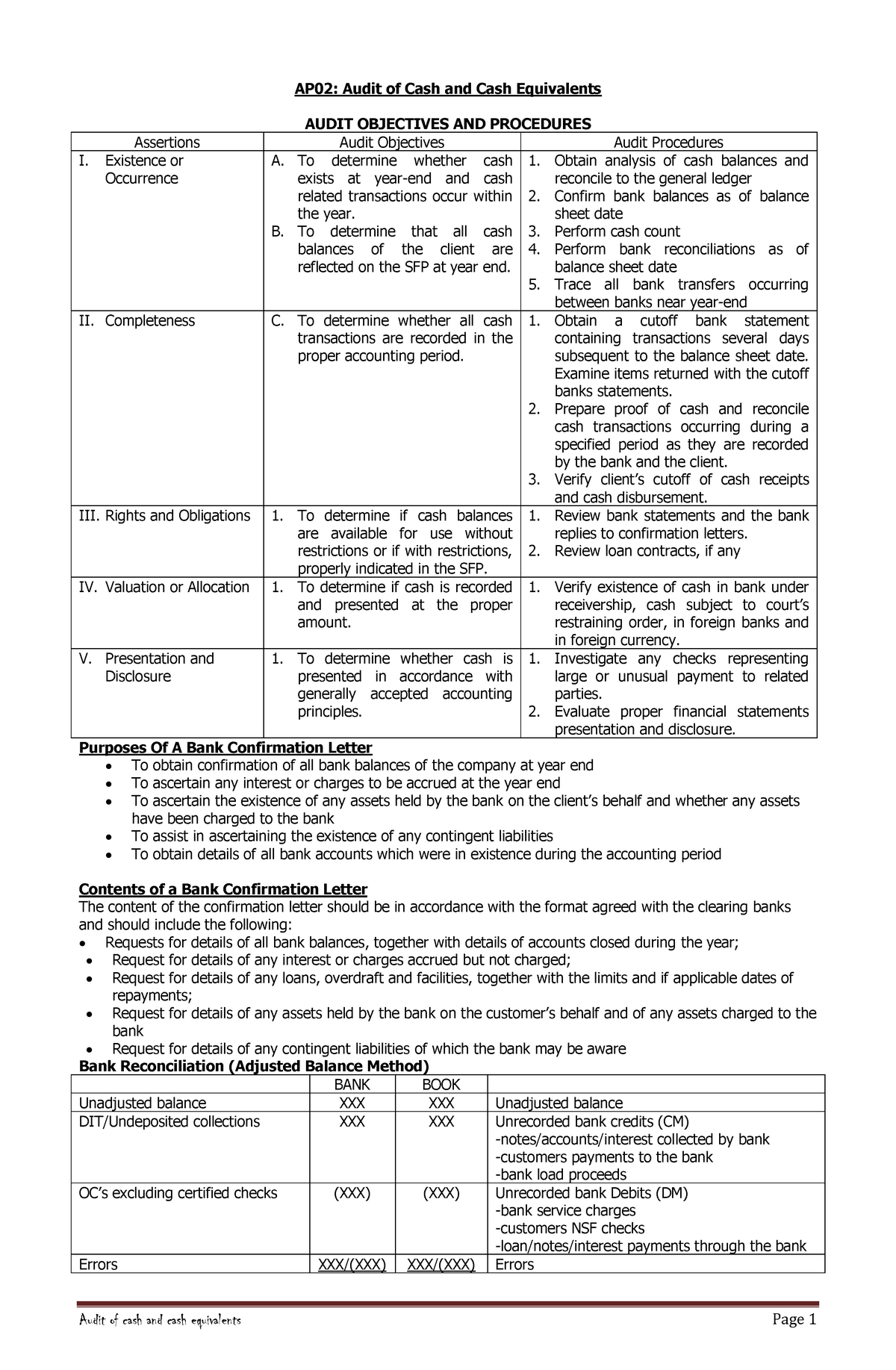

Full PDF Package Download Full PDF Package. The first important task for the auditor is to get a clear understanding of the clients policy and procedure for cash and bank. Recorded balances exist and are owned by the institution.

Cash and cash equivalents tend to be one of the first areas assigned to new auditors since it tends to be straightforward with less complexity and risk as other areas. Checklist Provide cash and cash equivalents faster than usual. In this role as an external auditor of company ABC ie as a.

Petty cash fund including. 625 The primary audit objectives for cash are to obtain reasonable assurance that. Key Audit Procedures for Cash and Bank Audit.

This will help the. In the audit of cash we usually test the audit assertions included in the table below. This video lecture discusses the audit of cash and cash equivalents particularly the substantive procedures to be performed on the said line item.

Adhere to general principles for cash control. Hello welcome to your new role. Audit Assertions for Cash.

AUDIT OF CASH AND CASH EQUIVALENTS SUBSTANTIVE AUDIT PROCEDURES FOR CASH Cash Balances Existence. CHAPTER 3 - Audit of Cash Cash Equivalents Problem 1 The CASH account of Don Corporations ledger on December 31 2006 showed the following. Cash recorded on the books exist - Count cash on hand-.

Sending Confirmations to all the bank accounts either physically or electronic means like. Account for all cash. A primary substantive procedure for cash is confirmation of the balances of the companys accounts with financial institutions.

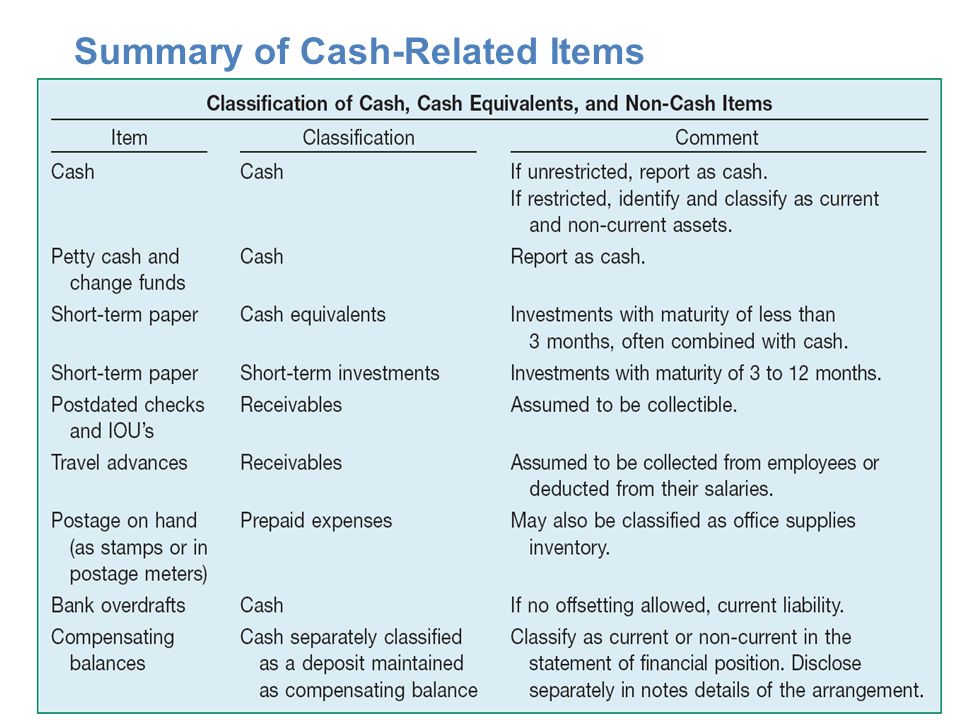

In Cash and Cash Equivalents there are two separate components. AUDITING CASH CASH EQUIVALENTS. Cash and cash equivalent are the most liquidated assets on the financial statement.

Cash balances on the balance sheet really exist at the reporting date. The following are the substantive audit procedures for cash. The objective of this template is to ensure the Completeness Accuracy Existence and Valuation of cash and cash equivalents.

Up to 3 cash back Scribd is the worlds largest social reading and publishing site.

Audit Of Cash And Cash Equivalents Existence Or Occurrence A To Determine Whether Cash Exists At Studocu

How To Audit Cash And Cash Equivalents Basic Audit Procedures

Cash Audit Procedures Assertions Objectives Management Cash Exists Include All Transactions That Should Be Presented Represents Rights Of The Entity Ppt Download

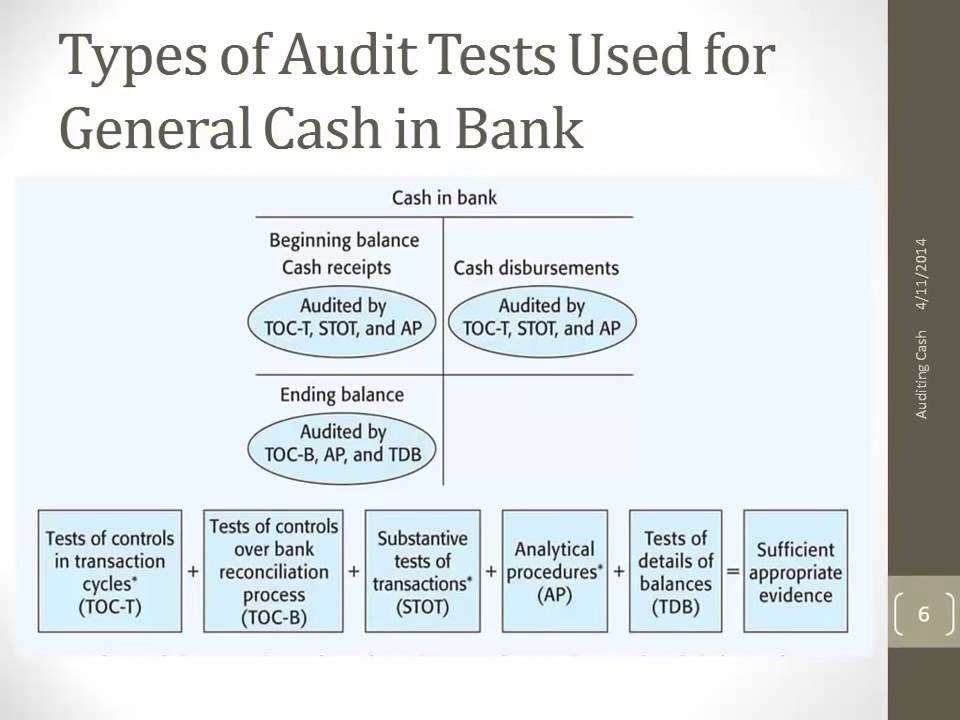

Types Of Audit Tests Used For General Cash In Bank Youtube

No comments for "Audit Procedures for Cash and Cash Equivalents"

Post a Comment